Banks Are Obsolete:

The Entire Parasitic Sector Can Be

Eliminated

by Charles Hugh Smith

What else can we do with the $1.25

trillion we'll save by eliminating these obsolete financial middleman

parasites? A lot.

Technology

has leapfrogged the banking sector, rendering it as obsolete as buggy whips. So why

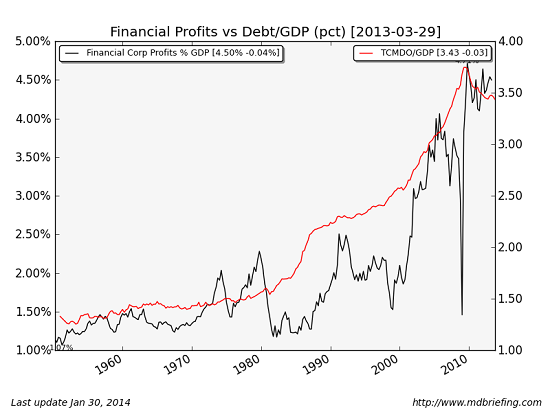

are we devoting 9% of our economy to an obsolete parasite? Financial sector profits now total

a staggering 4.5% of GDP (gross domestic product), while the expenses generated

by financial churning account for another 4.5% of the economy.

chart courtesy of Market

Daily Briefing

Software

and existing non-Wall Street/too-big-to-fail institutions could replace the

entire Wall Street/banking sector and drop costs to .5% of GDP, saving us 8+% of our GDP

($1.25 trillion) that is currently siphoned off by parasitic middlemen. The

banking sector is Exhibit A in the Middleman-Skimming

Economy (February 11, 2014).The pull of habit and propaganda is so strong that most people haven't even recognized that software and the Web can replace the entire financial/banking sector for a fraction of the cost of the current parasitic system, a system that (as we all know) has captured the regulatory and governance machinery of the central state, making a mockery of democracy.

The benefits of eliminating the financial/banking sector are immense and far-reaching.

What exactly do banks do? Banks perform these basic functions:

1. They hold depositors' money.

2. They act as a clearing house for payments, transferring funds from payer to payee.

3. They issue loans on a fractional reserve basis, i.e. a few dollars in cash deposits supports $100 in loans.

4. They originate and trade derivatives, run high-speed trading desks, operate various money-laundering and embezzlement schemes, influence elected officials with lobbying and campaign contributions and subvert both free market capitalism and democracy at every turn.

This entire parasitic middleman sector could be replaced with automated digital clearing houses and crowdfunded or non-bank loans. Why do we need banks to pay bills online? We don't; any clearing house could charge a small fee for the transaction.

Why do we need banks when loans can be crowdfunded? If we can invest money in start-ups via Kickstarter, Indiegogo, RocketHub, AngelList, etc., why can't we own a piece of someone's auto loan or home mortgage?

The web and software now enable the elimination of the entire middleman skimming operation of banking. Those with capital can invest that capital directly in loans that the investors choose. Risk is distributed throughout the system, and the process of verifying credit scores, income, valuations, assets, and so on--the building blocks of risk assessment and a market for debt and cash--can also be automated.

The entire notion that 100 savers put their money in a bank which then buys a mortgage with their savings and sells it as a security that supports a pyramid of derivatives is obsolete. Each saver can directly own (and sell on a transparent market) a piece of a mortgage, auto loan, business loan, etc. There is no need for a middleman banking sector at all--no skim, no concentration of risk, no opportunities for selling derivatives to unwary investors. All that goes away with the banking sector.

But what about holding deposits? We already have two institutions that could serve this role: credit unions and the post office. If those holding depositors' cash do not issue loans, they have no source of income to defray operating expenses. The solution is obvious: charge fees for holding deposits and payer-payee transactions.

If the fee structures are transparent, those who charge too much will disappear as customers go elsewhere. That's the purpose of transparent competition in an open marketplace.

Many other advanced nations have long combined postal and simple banking services: France and Japan come to mind. Here we have a postal service that is struggling to fund its operations in the era of email, and here we have millions of people who prefer to (or have to) do simple banking in person. There is no technical or administrative reason that the post office could not operate as it does in Japan, as a place to deposit funds (including auto-deposit of Social Security checks), take out cash, etc.

Please note that what I am suggesting is a transparent open market for these services provided by a range of enterprises and institutions. Assemble a marketplace of local credit unions, the post office, enterprises that handle payor-payee transactions such as Dwolla and PayPal, and you have a wide spectrum of choices to suit every need.

As for business loans: you can get small-business loans on PayPal right now. It's called Working Capital, and the borrower is given the total amount due right up front.

As for the commercial paper market: there is no technical reason why a transparent exchange couldn't enable borrowers and owners of capital to set short-term loan rates via transparent bidding with automated software.

The obsolescence of banking includes the Federal Reserve--the ultimate middleman skimming operation. But what about providing liquidity in credit panics? Well, to start with, once the banking sector is gone then the concentrations of risk and the obscuring of risk that go hand in hand with banking also disappear-- the forces that generate panics will have been dispersed. Those forces will have vanished along with the middleman financial sector that created all the risks, speculative excesses and panics. If there were a liquidity crisis, the Treasury could create and lend whatever funds were needed.

But what about manipulating interest rates and other forms of financial repression? Interest rates would be set by millions of borrowers and owners of capital in transparent transactions.

What about all those great investing services offered by big banks and Wall Street? As many have observed, automated index funds outperform 99% of fund managers over 10 year time frames. So Wall Street is also obsolete.

Once we get rid of these obsolete middleman parasites--Wall Street, the banking sector and the Federal Reserve--we have a delightful question to answer: what else can we do with the $1.25 trillion we'll save every year by eliminating these obsolete financial middleman parasites? A lot.

Why Banks Are Doomed: Technology and Risk

It's not just that banks are no longer needed--they pose a needless and potentially catastrophic risk to the nation. To understand why, we need to understand the key characteristics of risk.

The entire banking sector is based on two illusions:

1. Thanks to modern portfolio management, bank debt is now riskless.

2. Technology only enhances banks' tools to skim profits; it does not undermine the fundamental role of banks.

The global financial meltdown of 2008-09 definitively proved riskless bank debt is an illusion. If you want to understand why risk cannot eliminated, please read Benoit Mandelbrot's book The (Mis)Behavior of Markets.

Technology does not just enable high-frequency trading; it enables capital and borrowers to bypass banks entirely. I addressed this yesterday in Banks Are Obsolete: The Entire Parasitic Sector Can Be Eliminated.

Unfortunately for banks, higher education, buggy whip manufacturers, etc., monopoly and propaganda are no match for technology. Just because a system worked in the past in a specific set of technological constraints does not mean it continues to be a practical solution when those technological constraints dissolve.

The current banking system is essentially based on two 19th century legacies. In that bygone era, banks were a repository of accounting expertise (keeping track of multitudes of accounts, interest, etc.) and risk assessment/management expertise (choosing the lowest-risk borrowers).

Both of these functions are now automated. The funny thing about technology is that those threatened by fundamental improvements in technology attempt to harness it to save their industry from extinction. For example, overpriced colleges now charge thousands of dollars for nearly costless massively open online courses (MOOCs) because they retain a monopoly on accreditation (diplomas). Once students are accredited directly--an advancement enabled by technology--colleges' monopoly disappears and so does their raison d'etre.

The same is true of banks. Now that accounting and risk assessment are automated, and borrowers and owners of capital can exchange funds in transparent digital marketplaces, there is no need for banks. But according to banks, only they have the expertise to create riskless debt.

It's not just that banks are no longer needed--they pose a needless and potentially catastrophic risk to the nation. To understand why, we need to understand the key characteristics of risk.

Moral hazard is what happens when people who make bad decisions suffer no consequences. Once decision-makers offload consequence onto others, they are free to make increasingly risky bets, knowing that they will personally suffer no losses if the bets go bad.

The current banking system is defined by moral hazard. "Too big to fail" also means "too big to jail:" no matter how criminal or risky the bank managements' decisions, the decision-makers not only suffered no consequences, they walked away from the smouldering ruins with tens of millions of dollars in personal wealth.

Absent any consequence, the system created perverse incentives to pyramid risky bets and derivatives to increase profits--a substantial share of which flowed directly into the personal accounts of the managers.

The perfection of moral hazard in the current banking system can be illustrated by what happened to the last CEO of Lehman Brother, Richard Fuld: he walked away from the wreckage with $222 million. This is not an outlier; it is the direct result of a system based on moral hazard, too-big-to-jail and perverse incentives to increase systemic risk for personal gain.

And who picked up all the losses? The American taxpayer. Privatize profits, socialize losses: that's the heart of moral hazard.

Concentrating the ability to leverage stupendous systemic bets in a few hands leads to a concentration of risk. Just before America's financial sector imploded, banks had pyramided $2.5 trillion in dodgy mortgages into derivatives and exotic financial instruments with a face value of $35 trillion--14 times the underlying collateral and more than double the size of the U.S. economy.

In a web-enabled transparent exchange of borrowers bidding for capital, the risk is intrinsically dispersed over millions of participants. Not only is risk dispersed, but the consequences of bad decisions and bad bets fall solely to those who made the decision and the bet. This is the foundation of a sound, stable, fair financial system.

In a transparent marketplace of millions of participants, a handful of participants will be unable to acquire enough profit to capture the political process. The present banking system is not just a financial threat to the nation, it is a political threat because its outsized profits enable bankers to capture the regulatory and governance machinery.

The problem with concentrating leverage and moral hazard is that risk is also concentrated. And when risk is concentrated rather than dispersed, it inevitably breaks out of the "riskless" corral. This is the foundation of my aphorism: Central planning perfects the power of threats to bypass the system's defenses.

We can understand this dynamic with an analogy to bacteria and antibiotics. By attempting to eliminate the risk of infection by flooding the system with antibiotics, central planning actually perfects the search for bacteria that are immune to the antibiotics. These few bacteria will bypass the system's defenses and destroy the system from within.

The banking/financial sector claims to be eliminating risk, but what it's actually doing is perfecting the threats that will destroy the system from within. Another way to understand this is to look at what happened to home mortgages in the runup to the meltdown of 2008: the "safest" part of the financial sector ended up triggering the collapse of the entire pyramid of risk.

Once we concentrate risk and impose perverse incentives and moral hazard as the foundations of our financial/banking system, then we guarantee the risk will explode out of whatever sector is considered "safe."

Once you eliminate the "risk" of weak bacteria, you perfect the threat that will kill the host.

The banking sector cannot be reformed, for its very nature is to concentrate systemic risk and moral hazard into breeding grounds of systemic collapse. The only way to eliminate the threat posed by banks is to eliminate the banks and replace them with transparent exchanges where borrowers and owners of capital openly bid for yield (interest rates) and capital.

Bankers (and their fellow financial parasites) will claim they are essential and the nation will collapse without them. But this is precisely opposite of reality: the very existence of banks threatens the nation and democracy.

One last happy thought: technology cannot be put back in the bottle. The financial/banking sector wants to use technology to increase its middleman skim, but the technology that is already out of the bottle will dismantle the sector as a function of what technology enables: faster, better, cheaper, with greater transparency, fairness and the proper distribution of risk.

There may well be a place for credit unions and community banks in the spectrum of exchanges, but these localized, decentralized enterprises would be unable to amass dangerous concentrations of risk and political influence in a truly transparent and decentralized system of exchanges.

From Of Two Minds @ http://charleshughsmith.blogspot.ro/2014/02/banks-are-obsolete-entire-parasitic.html and http://charleshughsmith.blogspot.ro/2014/02/why-banks-are-doomed-technology-and-risk.html

For more information about the surrealist 'reality' of banking see http://nexusilluminati.blogspot.com/search/label/banksters

- See ‘Older Posts’ at the end of each section

Hope you like this

not for profit site -

It takes hours of work every day

to maintain, write, edit, research, illustrate and publish this website from a

tiny cabin in a remote forest

Like what we do? Please give enough

for a meal or drink if you can -

Donate any amount and receive at least one New Illuminati eBook!

Please click below -

Xtra Images – http://www.whatdoesitmean.com/bro3.jpg

http://www.globalresearch.ca/wp-content/uploads/2013/03/bankster-chess.jpg

http://www.realfarmacy.com/wp-content/uploads/2013/07/bankster.jpg

http://theflyingcameldotorg.files.wordpress.com/2012/07/bankers-dont-go-to-jail.jpg

For further enlightening

information enter a word or phrase into the random synchronistic search box @ http://nexusilluminati.blogspot.com

And see

New Illuminati – http://nexusilluminati.blogspot.com

New Illuminati on Facebook - https://www.facebook.com/the.new.illuminati

New Illuminati Youtube Channel - http://www.youtube.com/user/newilluminati/feed

New Illuminati on Google+ @ https://plus.google.com/115562482213600937809/posts

New Illuminati on Twitter @ www.twitter.com/new_illuminati

The Her(m)etic Hermit - http://hermetic.blog.com

The Prince of Centraxis - http://centraxis.blogspot.com (Be Aware! This link leads to implicate &

xplicit concepts & images!)

DISGRUNTLED SITE ADMINS PLEASE NOTE –

We provide a live link to your original material on your site (and

links via social networking services) - which raises your ranking on search

engines and helps spread your info further! This site is

published under Creative Commons Fair Use Copyright (unless an individual

article or other item is declared otherwise by the copyright holder) –

reproduction for non-profit use is permitted & encouraged, if you

give attribution to the work & author - and please include a (preferably

active) link to the original (along with this or a similar notice).

Feel free to make non-commercial hard (printed) or software copies or

mirror sites - you never know how long something will stay glued to the web –

but remember attribution! If you like what you see, please send a donation (no

amount is too small or too large) or leave a comment – and thanks for reading

this far…

Live long and prosper! Together we can create the best of all possible

worlds…

From the New

Illuminati – http://nexusilluminati.blogspot.com

My Brothers and Sister all over the world, I am Mrs Boo Wheat from Canada ; i was in need of loan some month ago. i needed a loan to open my restaurant and bar, when one of my long time business partner introduce me to this good and trustful loan lender DR PURVA PIUS that help me out with a loan, and is interest rate is very low , thank God today. I am now a successful business woman, and I became useful. In the life of others, I now hold a restaurant and bar. And about 30 workers, thank GOD for my life I am leaving well today a happy father with three kids, thanks to you DR PURVA PIUS Now I can take care of my lovely family, i can now pay my bill. I am now the bread winner of my family. If you are look for a trustful and reliable loan leader. You can Email him via,mail (urgentloan22@gmail.com) Please tell him Mrs Boo Wheat from Canada introduce you to him. THANKS

ReplyDelete